Biometric payments are going mainstream, but something is missing

- Thought leadership

- 9 Minute Read

- Last updated 27/05/2026

Rising awareness is not translating into confidence among consumers

Key Insights

-

Familiarity with biometric payments is relatively high in both the UK and US, with 28% in each market saying they are “very familiar”. In the US, unfamiliarity has dropped from 46% in last year’s survey to 30%, showing a clear year-on-year increase in awareness.

-

A majority in both markets expect biometric payments to become common in the next 5 - 10 years (58% UK, 62% US), but trust does not follow.

-

The US is notably more skeptical overall, with lower trust in companies (37% vs 48% UK) and consistently higher concerns around privacy and data misuse.

-

Age is the clearest dividing line, with younger consumers more focused on data privacy and security risks, while older groups are questioning the value, usefulness and reliability of biometric payments.

-

Qualitative responses show a clear divide between openness and rejection, with strong reactions centered around security, control, accessibility and fairness.

Don't have time to read more now? Sign up to our newsletter to get the latest insights directly in your inbox.

Biometric payments, transactions authorized using fingerprints, facial recognition or iris scans, are designed to simplify how people pay in person: by removing the need for passwords or PINs, these systems offer a more direct way to authenticate payments at the checkout, removing friction at the point of sale.

In 2024, Aevi first explored this space through a US-focused study of 2,000 adults. The findings highlighted a clear gap between awareness and adoption, with security and privacy concerns emerging as the main barriers to wider use.

This latest research builds on that analysis, expanding the study to more than 3,000 adults across the UK and US, looking at how familiarity, trust and hesitation have evolved, as well as how the two key markets differ across these areas.

We found a consistent tension: consumers increasingly expect biometric payments to become part of everyday life, but trust in the systems and organizations behind them has not kept pace.

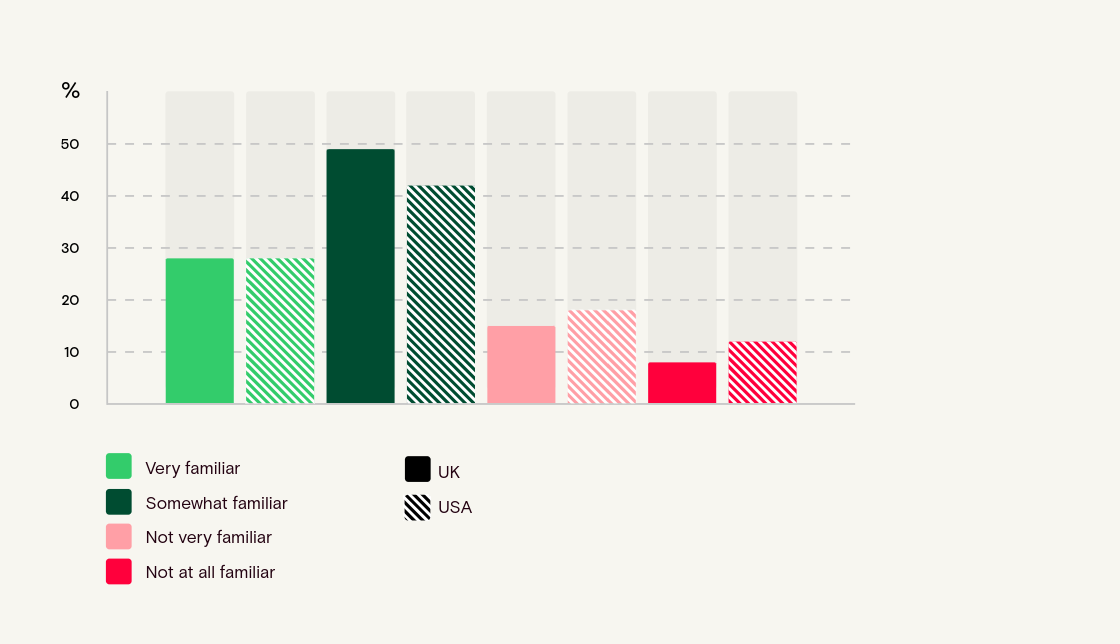

How familiar are you with biometric payment authorization methods (e.g. fingerprint, facial recognition, iris scan)?

Familiarity with biometric payments across the US and UK

Across both markets, familiarity with biometric payment authorization is relatively widespread: in both the UK and US, 28% of respondents say they are “very familiar” with methods such as fingerprint, facial recognition or iris scan payments, however, most respondents lie in the middle. In the UK, 49% say they are “somewhat familiar”, compared with 42% in the US, the US also has a slightly higher unfamiliar group overall, with 30% saying they are either “not very familiar” or “not familiar at all”, compared with 23% in the UK.

This shows that while biometric payments are becoming more widely recognized, many consumers still lack a clear understanding of how the systems work, how data is handled, and what protections are in place.

Somewhat expectedly, age is where the clearest patterns start to appear. Familiarity is most evident among younger respondents steadily declining with age in both markets. In the UK, 18 - 24s stand out, with 77% saying they are “very familiar” while in the US, familiarity peaks among 25 - 34s, where 45% say they are very familiar.

By 65+, unfamiliarity becomes much more prominent. In the US, 55% of over-65s say they are either “not very familiar” or “not familiar at all”, compared with 49% in the UK.

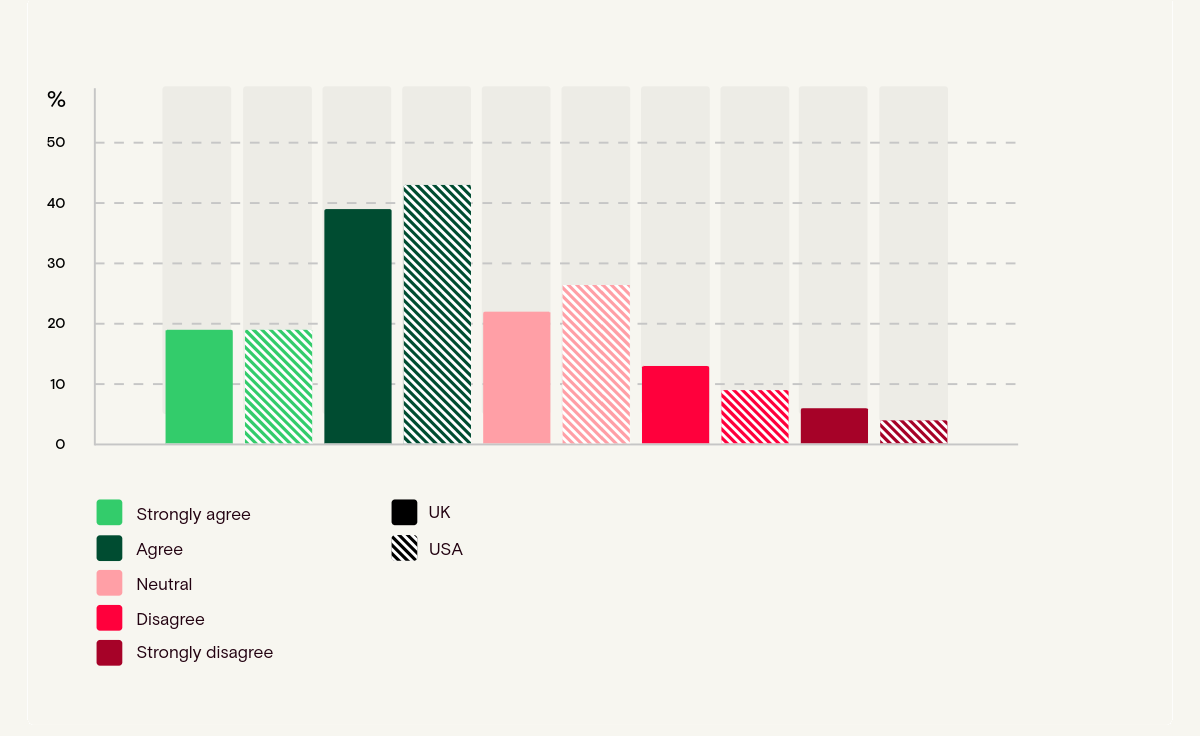

I believe using biometric payments will become one of the most common ways to pay for goods and services in person in the next 5 to 10 years.

A majority of respondents across both markets believe biometric payments will become one of the most common ways to pay for goods and services in person within the next 5 to 10 years. In the US, 62% agree or strongly agree, compared with 58% in the UK.

Expectations for the future adoption of biometric payments in the US and UK

Consumers expect biometric authentication to become the norm in the future, but this expectation reflects inevitability rather than enthusiasm.

Across age groups, belief in mainstream adoption remains fairly steady, but older respondents are more likely to move into neutral territory, in the US, neutrality rises from 20% among 25 - 34s to 34% among over-65s, a pattern suggesting older consumers are less convinced rather than strongly opposed.

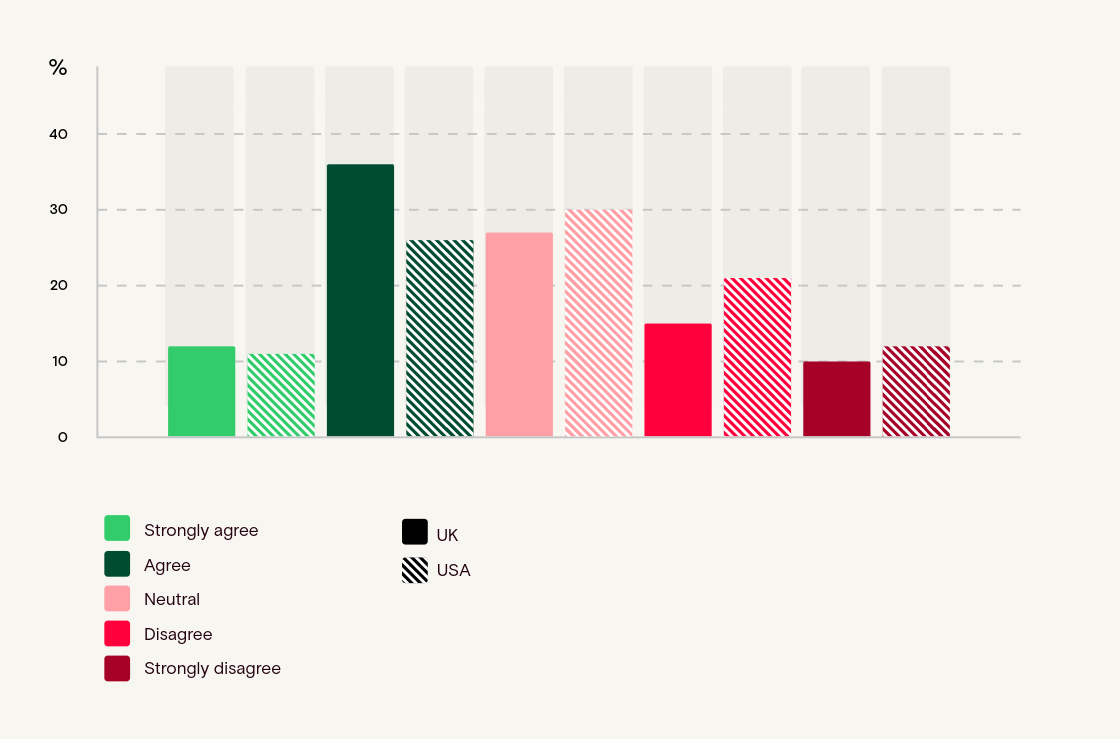

To what extent do you agree or disagree with the following statement: “I trust companies to protect my biometric data.”

Trust in companies to protect biometric data across the US and UK

Trust is where the story becomes more complicated.

Whereas in the UK, 48% of respondents agree or strongly agree that they trust companies to protect their biometric data, in the US, that falls to 37%, meanwhile, the US also shows higher levels of disagreement (and neutrality), indicating a more skeptical and less trusting baseline.

This gap matters because biometric payments rely on trust in how highly personal, and often irreversible, data is handled, unlike card numbers or passwords, biometric data cannot be easily changed once compromised.

Age once again plays a major role: younger UK respondents are particularly positive as 68% of UK 18 - 24s agree or strongly agree that they trust companies to protect biometric data, though this confidence drops sharply with age.

The US is more cautious from the get-go, even among US 18 - 24s, only 30% agree or strongly agree, while 40% disagree or strongly disagree whereas across older US groups, neutrality remains high, and trust never reaches the same levels seen among younger UK respondents.

In short, expectation of widespread adoption does not equate to trust in the infrastructure supporting biometric payments.

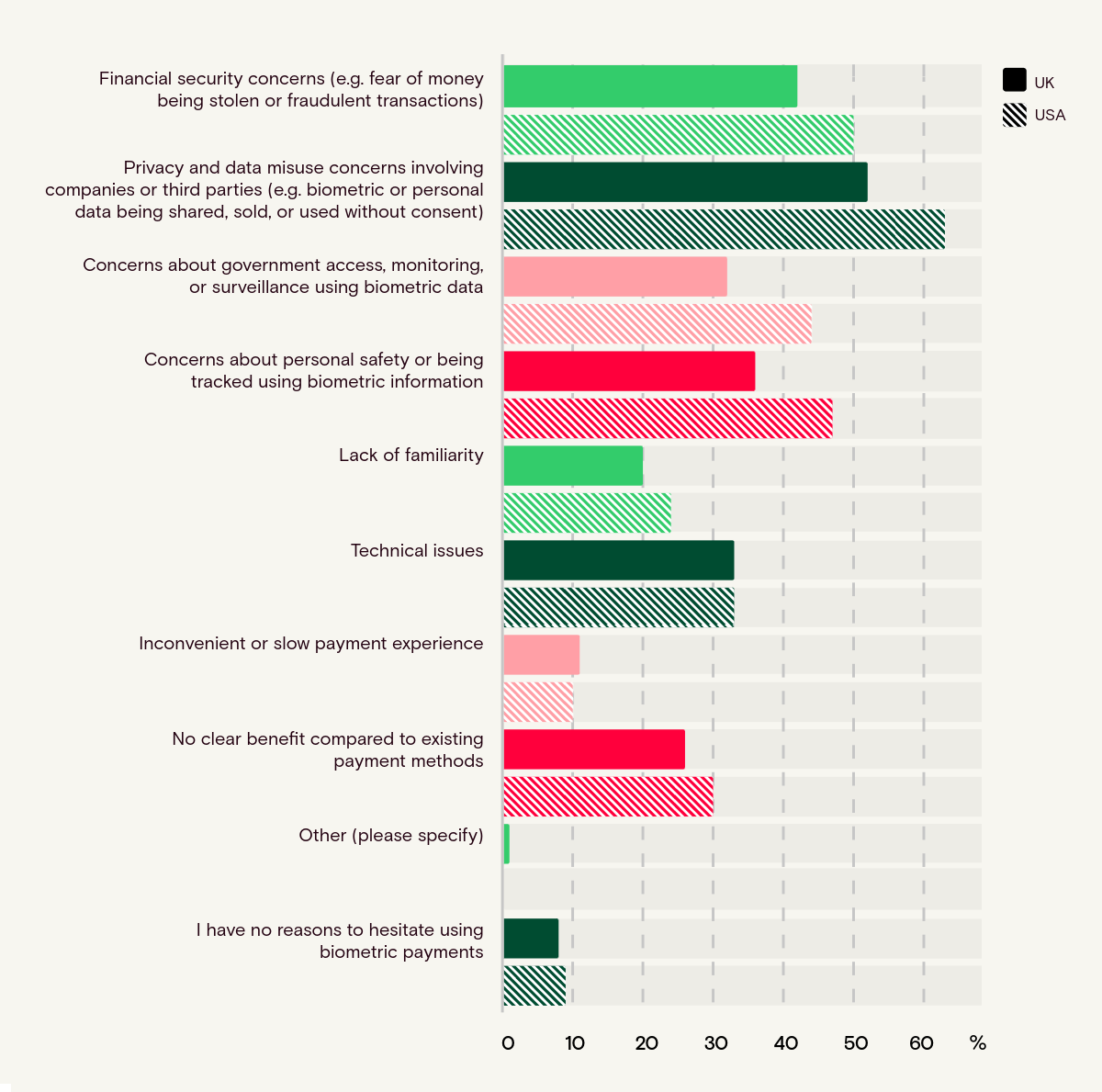

What are the main reasons, if any, why you would hesitate to use biometric payments?

When looking at what drives hesitation, we found that privacy and data misuse emerged as the clearest concerns.

In the US in particular, privacy and data misuse concerns are consistently high across every age group and represent a clear majority, ranging from 58% to 66%. In the UK, the same concern remains strong but overall lower, from 45% to 54%.

Reasons for reluctance to use biometric payments by age group in the US and UK

Financial security concerns are also high across both markets: in the US, concern remains stable across age groups, between 47% and 53%, in the UK, it is more varied, but still a major factor.

Fears around government access to biometric data, including fears of monitoring or surveillance, are far more prevalent in the US. The gap between markets is very clear, with 40% to 47% of US respondents citing this concern across all age groups, compared with 23% to 37% in the UK.

Such a pattern of concerns, particularly around privacy, data misuse and government access, points to a broader trust issue:

At the core of consumers’ concerns is control over their biometric data, where it is stored, how it is used, and who else might access it. In the US, these concerns run deeper, suggesting biometrics are tapping into wider anxieties around institutions, data use and oversight beyond payments alone.

The most interesting age pattern is how the reasons for hesitation shift with age.

In both markets, younger respondents are more focused on data risks, including privacy, security, tracking and misuse, while older respondents increasingly question whether biometric payments offer enough value in the first place.

Clearly, adoption barriers are not uniform and for younger consumers, the question is often: “Can I trust you with my data?” whereas for older consumers, it becomes: “Why do I need this at all?”

Behind the numbers. How people really see it

The open-text responses added very important depth and context to the findings. Across both markets, a significant share of respondents express firm resistance, with many stating that nothing would convince them to trust biometric payments.

This sentiment was not passive uncertainty but a clear rejection of the technology, rooted in deep skepticism and a lack of understanding of how biometric systems work.

Among those who are more open, expectations are at times almost impossibly high with many expressing scenarios of complete security and guarantees to follow.

Trust is conditional on stronger security, transparent data handling, clear consent mechanisms, visible regulation, and greater clarity around how companies handle biometric data particularly in the UK, while in the US a distrust in the government’s handling of data was more prominent.

Many respondents also emphasize the need for systems to prove themselves over time through consistent and reliable performance. In practice, this often translates into demands for near-perfect security standards, this highlights a chasm between what consumers expect and what technology can realistically guarantee.

United Kingdom

“If security was 100 percent secure.”

“Security and change the biased of facial recognition”

“Often when using biometrics, I find I have to try twice or more to get a payment to go thorough, which can be annoying”

“I think it would have to be regulated and proven to be trustworthy before I use it.”

“If the data is guaranteed to be stored locally and in an encrypted format and not uploaded to servers, I would be more reassured”

“I can see it will be the way to go. How would the system cope with someone who has failing sight or developing cataracts? I wouldn't fully trust biometrics.”

United States

“Our government has proven time and time again how it cannot be trusted. On a business level, corporations have also proven time and time again they can’t be trusted, they are also careless and seem to get hacked for information frequently. I would not trust this at all.”

“Companies need to be more trustworthy. They sell data way too willingly”

“It should be installed total security identity protection on payment terminals”

“Technology needs to be tested thoroughly and safeguards for data put into place.”

“I would need to see it being used consistently and successfully”

“The lack of information sharing is too risky and companies failed to protect the public many times before.”

Accessibility and bias need deeper attention

The qualitative responses also reveal concerns that sit beyond standard security and privacy themes.

Some respondents raise practical accessibility questions, including what happens if a biometric identifier changes, fails, or cannot be captured reliably. Examples include failing eyesight, cataracts, facial changes, finger injuries, unreliable fingerprints, or devices that do not work consistently. Others raise concerns around bias and accuracy, particularly facial recognition bias and whether biometric systems work equally well for everyone.

These comments may not represent the dominant quantitative finding, but they are extremely important as they show that trust is not ‘only’ about cybersecurity, that there may be some practical and often overlooked aspects that genuinely pose the challenge of whether biometric payment systems are currently perceived as fair, fully inclusive and reliable in real life.

Conclusions

This research highlights a clear and familiar tension in the evolution of payment technology. Consumers broadly expect biometric payments to become part of everyday life, yet trust in the systems and organizations behind them remains limited. That expectation is driven more by a sense of inevitability than by confidence.

That gap is particularly visible when comparing the two key markets: the US consistently shows higher levels of skepticism, especially around privacy, surveillance, and institutional trust, pointing to concerns that extend beyond payments alone. The UK, while not without hesitation, follows a more gradual trust curve, with younger consumers in particular appearing more embedded in biometric technologies, though still far from fully trusting them.

Age remains the most consistent driver of attitudes. Younger consumers tend to question how their data is handled and who controls it, while older groups are more likely to question the value and relevance of biometric payments altogether. Across both segments, resistance is not rooted in usability or convenience, but in control, security, and trust.

As Aevi CEO Mike Camerling explains:

“As we’ve seen across our more recent consumer research, whether it’s about agentic commerce to digital currencies in in-person payments, control and trust remain consistent pressure points. Biometrics lands firmly within that same pattern. The technology itself might not be the barrier, but how it’s understood clearly is…how transparently it operates, and how much control people feel they retain.”

Back in 2024, Camerling highlighted one of the biggest challenges facing biometric payments: education and trust.

It’s difficult for small retailers to make the case for biometrics because they don’t have the reach or budget, in most cases, to reach the public and educate them. It will take businesses from across the payment sector to demonstrate the safety and efficacy of this technology for public confidence in it to continue to grow and for deployment of it to increase."

Our latest research suggests that assessment still holds true today, and in some areas, especially across the US, the challenge has only become more pronounced.

The qualitative responses reinforce this dynamic. A significant share of respondents reject biometric payments outright, while those who are open set extremely high expectations, often calling for near-perfect or even “unhackable” systems. In practice, this points to a trust threshold that may be difficult for the industry to fully meet, and highlights the scale of the challenge ahead.

For payment providers, banks, retailers, and technology partners, the implication is that adoption will not be driven by availability or speed alone. It will depend on whether biometric payments are designed to feel transparent, controllable, and genuinely beneficial. Consumers want clear data practices, visible consent, strong safeguards, fallback options, and a compelling reason to choose biometrics over existing methods.

This reflects a broader pattern seen across Aevi’s original consumer research, from earlier study on biometric payments adoption across the US to more recent analysis of the emerging agentic commerce technologies, the same themes consistently show up: trust, control, and visibility are the consumer’s own conditions for adoption. As in-person payments become more advanced, these factors are definitely becoming more important, not less.

Biometric payments may be moving closer and closer to mainstream use, but trust remains the critical infrastructure that has yet to be built.

Methodology:

This report draws on a survey of more than 3,000 adults across the United Kingdom and the United States, exploring attitudes toward AI-driven and agentic commerce in payments. The sample was balanced across key demographics, including age and gender, to ensure broad representativeness across both markets.

Alongside the quantitative analysis, the study also incorporated open-ended responses from participants. Nearly 3,000 qualitative comments were examined to identify recurring themes, including the use of phatic and emotionally expressive language around trust, control, and autonomy in payments.

Interested in reading more around this subject? Here are some useful articles…