5 key trends transforming convenience stores and gas stations

- Thought leadership

- 8 Minute Read

- Last updated 09/06/2026

The future of gas stations and the future of convenience stores is becoming faster, more connected and far less reliant on the traditional checkout. From self-service kiosks and smarter POS technology to alternative payment methods across the forecourt and in-store journey, payments are becoming increasingly distributed and embedded into the customer experience.

Key Insights

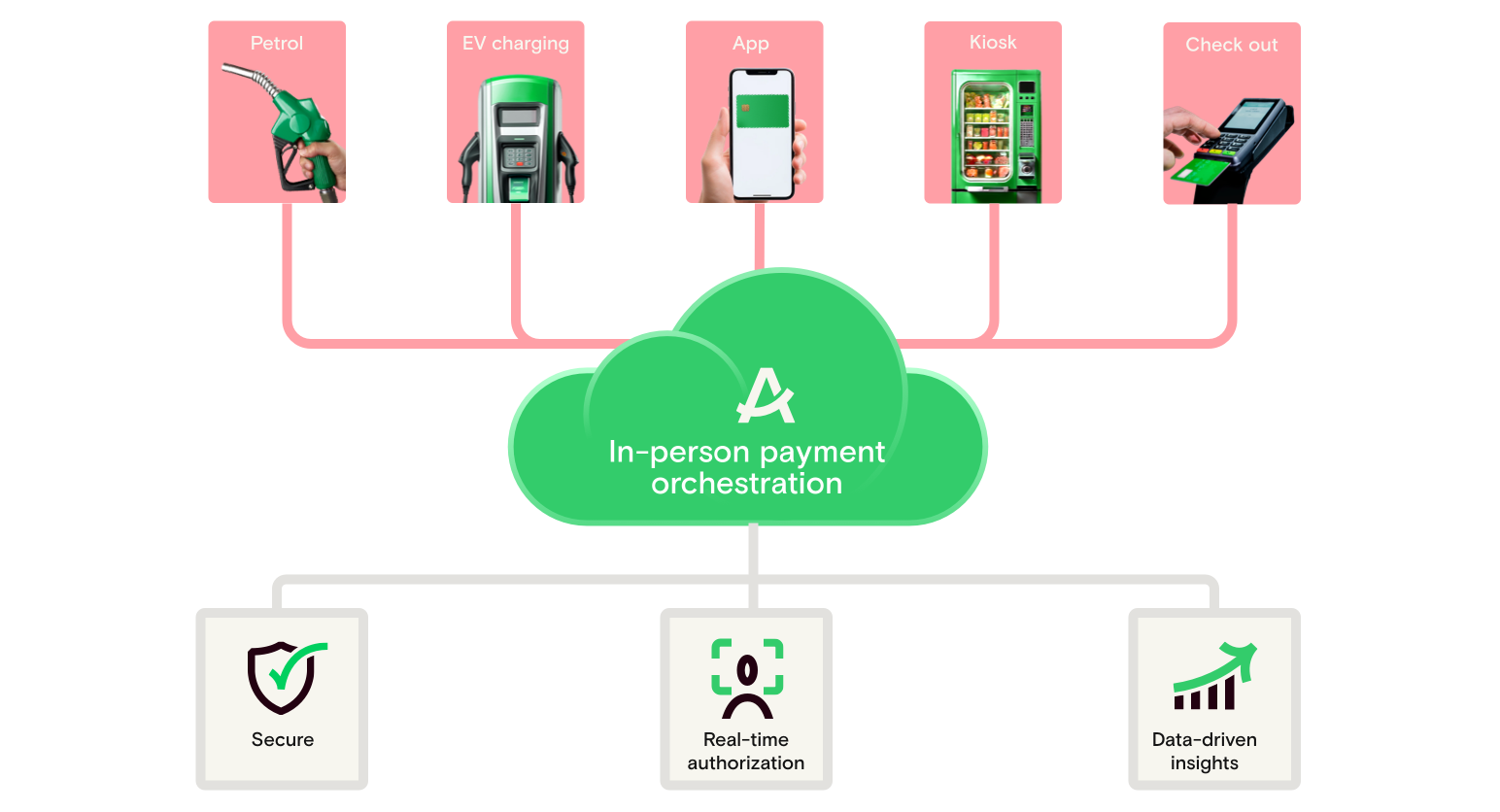

- Convenience stores are expanding payments across pumps, kiosks, mobile and in-store checkout to support faster, more flexible journeys.

- Self-ordering kiosks reflect a wider move toward distributed, self-service payments, with clear implications for the future of convenience stores.

- The future of retail payments here is less about new tech and more about removing friction from frequent, low-margin transactions.

- Trust remains central as more stores introduce unattended, automated and self-service payment journeys.

- Payments are becoming embedded into the journey itself, with fuel, food and checkout blending into one connected experience that helps define the future of gas stations.

Don't have time to read more now? Sign up to our newsletter to get the latest insights directly in your inbox.

On paper, convenience stores and gas station forecourts should be in a good position...

…Busy locations, frequent visits, and customers who value speed. In reality, most forecourts are fighting on multiple fronts - rising operating costs, increasingly demanding, price-sensitive shoppers, staff shortages, changing fuel demand, and a wave of new compliance and security requirements.

At the same time, the forecourt itself is changing, from a simple fuel stop into a more connected, multi-use environment where unattended payments and more flexible customer journeys are becoming the norm.

That mix is forcing operators to rethink everything from site formats and what they offer in-store, to how they handle payments at the pump, in‑store, and on mobile. As a result, many forecourts are investing in new technologies and payment experiences that can adjust quickly as customer behavior continues to change.

Here are five key trends transforming convenience stores and gas stations today.

1. EMV, PCI, and fraud risk are back on the agenda

A lot of fuel and convenience operators feel like they “did EMV” years ago. The rollout across terminals and forecourts is largely complete, outdoor infrastructure has been upgraded, and the big retrofit cycle is behind them.

But risk has not disappeared with the rollout. PCI DSS 4.0 requirements, more sophisticated fraud patterns, and aging payment infrastructure are forcing operators to look again at systems that may have been deployed quickly under earlier deadlines.

The conversation now is whether existing setups still actually hold up.

Pumps or in-store devices that fall back to magstripe, lack contactless, or run on outdated software and legacy setups can leave operators carrying more risk when fraud happens, and that can also mean more disputes and more scrutiny from card networks and processors.

At the same time, customers now expect to tap a card or mobile wallet at the pump as easily as they do anywhere else.

Together, that’s turning EMV, PCI, and fraud control into a continuous, strategic topic, with forecourts reviewing legacy devices, reducing fallback reliance, and looking at how their payments stack can support stronger authentication, encryption, and contactless by default - all without slowing anything down.

2. EV charging and fuel demand are changing the forecourt

Fuel demand isn’t disappearing, but it is changing. More efficient vehicles, EV uptake, changing travel patterns, and uneven demand in certain regions are all taking some demand out of traditional gasoline and diesel - even as overall fuel consumption in the U.S. has declined by less than 1% annually over the last decade.

For fuel and convenience store operators, that means the forecourt can’t rely solely on fuel and must earn its keep through the overall basket and the experience they build around the pump.

“Taking a payment at the charger is only a small part of the challenge. What operators really need to think about is everything behind it — how that experience connects with their wider estate, from pumps and kiosks to in‑store and digital. As more touchpoints are added, complexity builds quickly across systems, partners and data, and that’s where value is often lost if it isn’t managed properly.”

Ghermaine Henry, Head of Fuel & Mobility EMEA, Aevi

EV charging is a big part of that. Drivers plugging in for 20-40 minutes behave differently than drivers filling up in a few minutes: they have more time to step inside, browse, grab something to eat or drink, and interact with digital offers. That creates new revenue opportunities (one 2026 study found that more than 90% of EV drivers make additional purchases while they charge) but also new expectations around how easy it is to pay and earn rewards, alongside how straightforward the move between charger, the store and any on-site apps or kiosks is.

What this all leads to is a more mixed setup. Forecourts are starting to plan for a more mixed energy future - with different pump and charger layouts, new services targeted at EV drivers, and a more connected forecourt-to-store experience - with payments at the center. We’ve written more about what that looks like in practice in our article on adopting new payment technologies at your petrol station.

The sites that can link those moments together, without slowing things down, will be better placed for what comes next.

3. More digital, more self‑service, more unattended

Customers are getting used to doing more themselves, whether that’s self‑checkout in grocery stores, ordering ahead on an app, or tapping a phone at a kiosk. Recent retail research on self‑service systems and self‑service technologies shows that this behavior is now firmly mainstream.

The same pattern is playing out in convenience and fuel. Wider retail data shows that by 2024, 84% of U.S. shoppers preferred self-service kiosks - with 66% choosing them over staffed checkouts.

For operators, self-service is a way to keep lines moving, make 24/7 trading viable, and cope with ongoing labor and wage pressure. Unattended payments and compact self-checkout are letting smaller sites add touchpoints without adding headcount - while still giving customers the speed and control they’re looking for.

The flipside is that tolerance for downtime and “card not accepted” messages is low. If a kiosk or pump doesn’t work first time, customers are likely to abandon the transaction and head elsewhere.

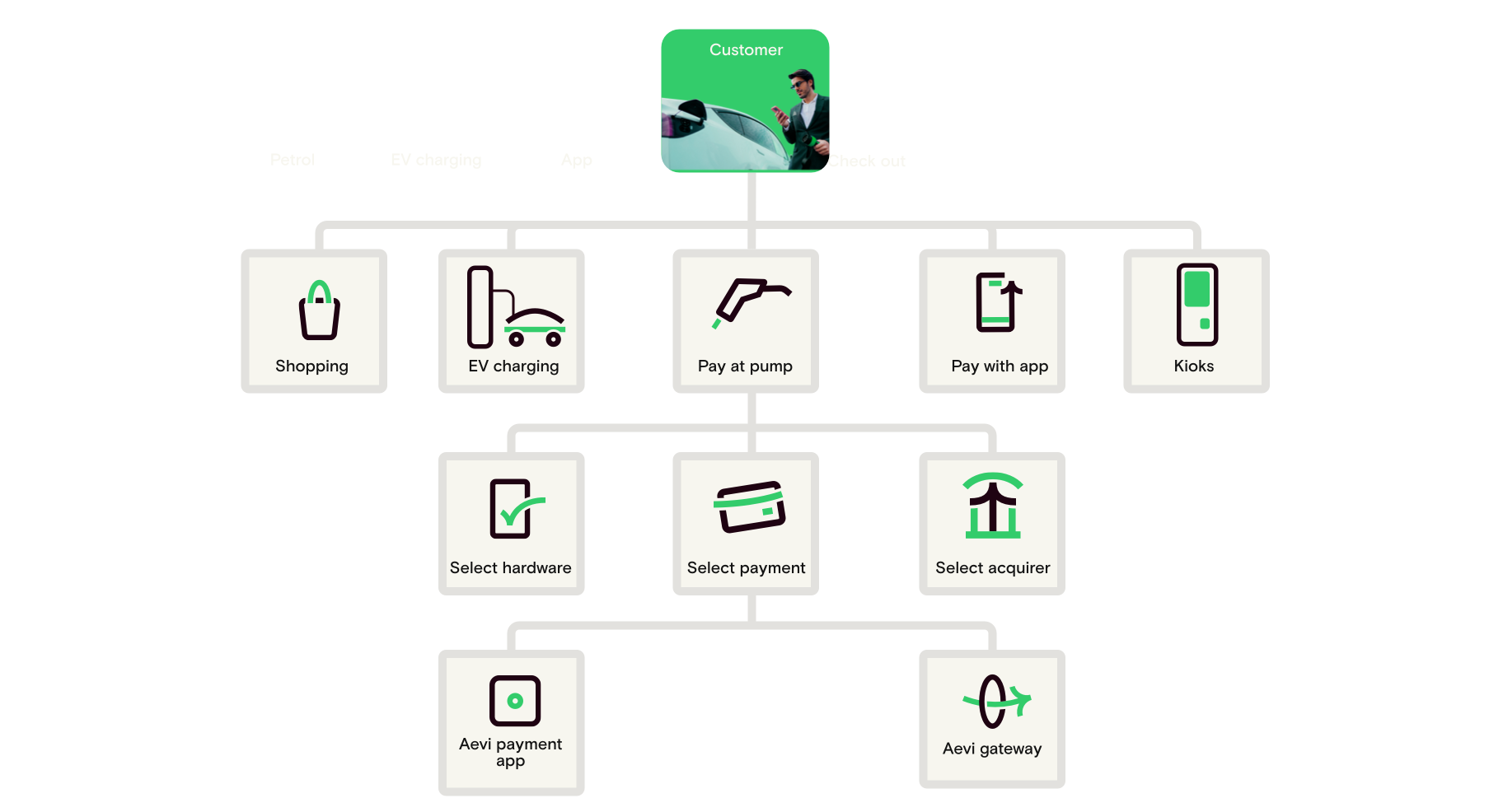

Because of that, more convenience store gas stations are bringing attended and unattended payments into a single model, often through a single payments platform that can run pumps, kiosks, and in‑store lanes.

They want all systems running on the same core payments infrastructure, with consistent reporting and security, and loyalty integrated in the background - so customers can move between them without thinking about how they’re paying.

Across the industry, these kinds of c-store industry trends are pushing operators toward more connected payment setups.

“Each new payment touchpoint adds value on the surface, but also complexity underneath. What operators often overlook is the need to keep everything connected, across systems, partners, and channels, so they don’t end up scaling fragmentation instead of experience.”

Ghermaine Henry, Head of Fuel & Mobility EMEA, Aevi

4. The forecourt visit is becoming a fuller stop

Fuel and charging still trigger most forecourt visits, but they’re increasingly the starting point, not the end of the story. What really moves the needle now is how many of those visits turn into “fuel plus something” - and how often customers build that into their routine.

That’s changing how forecourts are designed and used, with many new locations being planned and merchandized around coffee, hot food, quick everyday groceries, and simple services like parcel collection. The forecourt brings the footfall; the store is where you build value and set yourself apart from your competitor down the road.

Payments connect the two. If it’s easy to move from paying at the pump or charger into a quick in‑store checkout (whether that’s a staffed lane or self‑checkout) and loyalty can be earned or redeemed along the way, customers are much more likely to make that extra stop inside.

Forecourts that treat the journey as one continuous experience, with consistent payment experiences from outside to inside, are better placed to turn changing fuel and EV behavior into higher-value repeat visits.

5. A stable channel with a higher bar

On the surface, convenience in the U.S. looks remarkably stable. There are just under 152,000 stores, a slight decrease of 0.2% year‑on‑year, and the number of locations selling fuel has actually risen to its highest level in eight years. NACS/NIQ data shows that just over 80% of c‑stores now sell fuel, and they still handle roughly 80% of the fuel Americans buy.

But that doesn’t mean nothing’s changing. Weaker sites are dropping out, while stronger, better-located operators and larger groups keep expanding, upgrading formats, and leaning harder into food, coffee, and those other everyday essentials. The overall store count barely moves, but expectations of what a “good” site looks and feels like keep creeping up.

In that kind of market, it’s not enough to be the closest gas station with a store. Operators are being judged on the full package: how the site looks, what’s on offer, how quickly you can get in and out, and how simple it is to pay across fuel, EV, in‑store, and self‑service.

That’s why many are standardizing on a single payments orchestration layer to keep things consistent across every site and touchpoint.

It’s less about scale, more about how each site performs and how it stacks up against the one down the road.

What this means for the future of gas stations and convenience stores

All of this gives a pretty clear hint about the future of convenience stores and gas stations. The strongest sites will feel less like traditional forecourts and more like compact, efficient locations where people can refuel, pick up what they need, and pay in whatever way suits them - without it getting in the way of the visit.

For operators, that means treating payments and customer journeys as part of the same job. If you can keep removing friction between the pump, the store, and any self‑service touchpoints, you’re in a much better place to ride the next wave of convenience store trends and c‑store trends - whatever shape they take.

If you run a forecourt or fuel site and you’re looking at how payments can better support what’s happening on site, now’s the right time to talk. Get in touch with our team to see what a more connected approach could look like on-site.

Interested in reading more around this subject? Here are some useful articles…