Card-present vs. card-not-present transactions: What’s the real difference?

- Thought leadership

- 5 Minute Read

- Last updated 16/12/2025

Card-present transactions happen when the card is physically used at a terminal, while card-not-present transactions are completed remotely through online or app-based entry. That single difference affects fraud risk, fees, verification, and liability. Understanding both helps you choose the right payment mix, and build a setup that supports customers wherever they choose to pay.

Key Insights

-

Card-present (CP) payments are lower risk and typically cheaper because the card and customer are verified in person using EMV technology.

-

Card-not-present (CNP) payments drive reach and revenue, but require stronger fraud tools like CVV, AVS, tokenization, and 3-D Secure.

-

Verification, liability, and processing fees differ significantly between CP and CNP, impacting margins and operational complexity.

-

Merchants increasingly need both, and orchestration helps unify CP and CNP flows into one flexible, scalable payment strategy

Don't have time to read more now? Sign up to our newsletter to get the latest insights directly in your inbox.

Is the card physically used, or not?

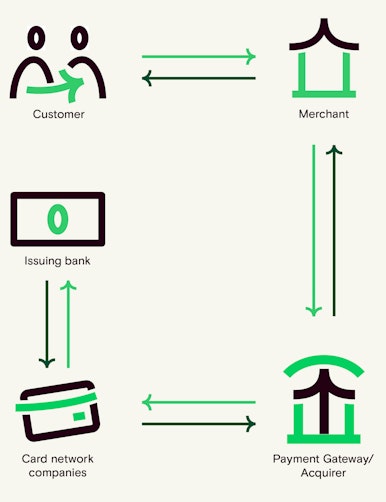

When businesses compare card present vs card not present transactions, they’re really asking one question: was the card physically used at the point of sale, or not?

That single detail shapes how payments are verified, how fraud is managed, how much you pay in processing fees, and who is liable when something goes wrong.

This guide breaks down the difference between card-present (CP) and card-not-present (CNP) transactions, what each means for your business, and how to choose the right mix across in-store and online channels.

What is a card-present transaction?

A card-present transaction happens when both the card and the cardholder are physically at the point of sale. The customer taps, inserts, or swipes their card or mobile wallet on a payment terminal, which reads the card’s chip and authenticates the transaction.

A CP transaction happens when the card and customer are physically in front of you. The card is tapped, dipped, or swiped on a payment terminal that reads the EMV chip and authenticates the payment. Because the terminal verifies the card and staff can confirm the cardholder, CP transactions carry lower fraud risk and usually come with lower processing fees.

Card-present payments also deliver (mostly) immediate approval, (however, technically, they still require online authorization unless the terminal is configured for offline approvals), fast throughput, and a familiar checkout experience. The main requirement is access to a terminal or mobile POS device with secure EMV and NFC (Near Field Communication) capabilities. For most businesses with in-person interactions, card-present is the simplest, safest, and most cost-efficient payment flow.

A little-known fact:

Even contactless payments are classed as card-present. They use the same secure EMV infrastructure and one-time cryptograms as chip-and-PIN, which means tap-to-pay is actually one of the safest ways to accept cards.

The most important thing to know:

Card-present transactions are almost always cheaper, safer, and easier to manage than their online equivalents. If you take payments face-to-face, CP should be your default acceptance method.

-

What CP means for you and your merchants:

- Lower fraud and fewer chargebacks

- Lower processing costs and better margins

- A fast, reliable in-person checkout

- Minimal friction and high customer trust

- Straightforward PCI compliance with secure terminals

What is a card-not-present transaction?

A CNP occurs when the card is, (you guessed it) not physically presented to the merchant. Instead of tapping or inserting a card, the customer enters their card details remotely, usually through an online checkout, mobile app, phone order, or, in some rare cases, mail order form. If you’ve ever typed in your card number, expiry date, and CVV code, you’ve completed a CNP payment.

CNP payments give businesses global reach, always-on sales, and the ability to grow beyond physical locations. They power ecommerce, digital subscriptions, bookings, and card-on-file experiences, making them a major driver of modern revenue growth.

Because these transactions happen remotely, they do carry higher fraud pressure and higher processing fees. That’s why merchants rely on verification methods like CVV, AVS, 3-D Secure, and tokenization to reduce disputes and keep customer journeys smooth.

A little-known fact:

Even follow-up charges, like monthly subscriptions or repeat billing remain classed as CNP, even if the first transaction happened in person. That means the ongoing risk profile stays higher, not lower.

The most important thing to know:

CNP transactions offer huge reach and convenience, but they also require tight fraud controls to keep costs stable and liability low. Strong authentication (like 3-D Secure) is what allows merchants to scale remote sales confidently.

-

What CNP means for you and your merchants:

- Access to global customers and truly 24/7 revenue

- Flexible sales models (subscriptions, bookings, digital services)

- Higher fraud exposure that needs stronger checks

- More chargebacks without the right authentication

- Greater reliance on PCI DSS-compliant gateways and tokenization

An easy-reference guide to the differences between CP & CNP

To make the differences easier to understand at a glance, here’s a complete side-by-side comparison of card-present vs card-not-present transactions. This table breaks down how each payment type works, how they’re verified, and what they mean for fraud, fees, liability, and compliance.

Aspect

Card & customer physically present?

How the payment happens

Verification methods

Fraud risk level

Common fraud types

Processing fees

Liability rules

Typical use cases

Speed & customer experience

Security controls

PCI compliance considerations

Operational requirements

Revenue impact

Best for

Card - Present (CP) Transaction

Yes, card and cardholder are both at the point of sale

Card is tapped, dipped (chip insert), or swiped on a terminal

EMV chip & PIN, chip & signature, and contactless. In many regions, contactless limits no longer apply when customer verification (PIN or biometrics) is automatically triggered, these rules vary by market.

Low, thanks to EMV chips and in-person checks

Stolen cards, rare counterfeit attempts, terminal tampering

Lower due to reduced risk

EMV liability shift applies; liability often moves to the party using less secure tech

Retail stores, cafés, restaurants, hospitality, transport, in-person services

Very fast; instant approval at POS

EMV chip, PCI-PTS approved terminals, tamper checks, staff training

Secure terminals, updated firmware, controlled device access

POS device, stable connection, staff oversight

Lower fraud losses and chargebacks; predictable costs

In-store, face-to-face, high-trust interactions

Card-Not-Present (CNP) Transaction

No, payment details are provided remotely

Customer enters card details online, in-app, by phone, or via mail order

3D Secure, CVV, AVS checks, device/browser signals, behavioral biometrics

High, stolen card numbers and phishing are common

Card-number theft, bots, phishing, account takeover

Higher due to offset fraud and chargebacks

In Europe, Merchants are usually liable unless 3-D Secure shifts responsibility. In the US, liability rules differ slightly between domestic and cross-border CNP transactions.

Ecommerce, mobile apps, phone orders, subscriptions, card-on-file billing

Fast but varies depending on fraud checks (e.g., 3DS)

PCI DSS gateway, tokenization, CVV/AVS checks, strong authentication

PCI DSS gateway, encrypted transmission, no storage of CVV, tokenization (“PCI compliance in card not present transactions”)

Online checkout, payment gateway, fraud tools

Higher fees and fraud exposure, but enables global reach and 24/7 sales

Remote sales, ecommerce, recurring payments, global customers

Once you understand how CP and CNP differ, it’s much easier to design a flexible, future-proof payment setup, (and to choose partners who help you scale it).

The future of CP and CNP (and what it means for you)

As customers move between online and in-store channels, the line between card-present and card-not-present is getting thinner. A shopper might browse online, buy through an app, and pick up in person. So the real question becomes: are your payment flows flexible enough to follow the customer wherever they choose to pay?

Mobile wallets, biometrics, tap-to-phone, and tokenized credentials are making both CP and CNP faster and more secure. And as these tools become standard, another question emerges: is your current setup designed to support these new behaviors, or is it holding you back?

Whether you operate in person, online, or both, the opportunity is the same: build a payment environment that stays consistent, secure, and seamless no matter where a transaction starts or ends.

Orchestration platforms like Aevi help unify these experiences so you’re not managing two separate worlds, but one connected payment strategy.

Understanding the differences between CP and CNP is the first step. Knowing how to use both to support your customers is what keeps your business growing.

"Orchestration gives you one control layer that unifies card-present and card-not-present for our retailers, ISOs, ISVs, and financial institutions. The market has shifted from end-to-end bundles to best-of-breed stacks, and orchestration enables that shift. You choose the components you want, build your own stack, and keep full control across every channel. One set of rules, one view of the customer, and freedom to change providers without disrupting your estate. It turns payments into a modular system you can adapt as your business grows."

Victor Padee, CRO, Aevi

Looking to simplify how your merchants manage card-present and card-not-present payments?

Let’s talk about how orchestration brings every payment channel together and gives you clearer visibility across your portfolio.

Interested in reading more around this subject? Here are some useful articles…