The rise of mobile payments: opportunities and challenges

- Thought leadership

- 5 Minute Read

- Last updated 08/10/2024

Key Insights

-

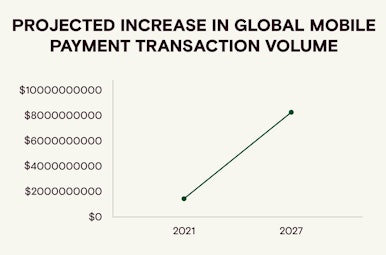

Mobile payment transactions are projected to skyrocket, from $1.44 trillion in 2021 to $8.26 trillion by 2027, driven by global wallets like Apple Pay, Alipay, and domestic schemes like Giropay and Payback.

-

Mobile payments enable global reach, a seamless customer experience, and valuable data insights, while offering increased security through encryption and tokenization.

-

Developers and businesses must navigate compatibility issues, rising fraud risks, and evolving regulations, while preparing for future shifts shaped by AI, blockchain, and industry consolidation.

Don't have time to read more now? Sign up to our newsletter to get the latest insights directly in your inbox.

Mobile payments have evolved from a futuristic concept to an integral part of our daily transactions. Whether you're a developer planning to integrate mobile payments into your app or a product manager tasked with implementing the latest mobile POS (Point of Sale) system, the rapid growth of mobile payment systems presents both exciting opportunities and significant challenges.

In this article, we’ll explore what mobile payment systems are, how they work, and what to consider when adopting this game-changing technology.

What is a mobile payment?

At its core, mobile payments involve using a mobile device to transfer funds. This includes global wallets like Apple Pay, Alipay, and PayPal, which enable contactless payments in-store or online. Additionally, domestic mobile payment schemes, such as Giropay and Payback in Germany or Paysera in the UK, are also gaining traction. The convenience and speed of these methods have driven widespread adoption.

-

Global mobile payment transaction volume reached $1.44 trillion in 2021, and it's projected to hit $8.26 trillion by 2027—a staggering growth rate that demonstrates the increasing shift towards cashless societies.

But mobile payments go beyond just tapping your phone at checkout. They also involve the backend systems and infrastructure that make these transactions possible.

How do mobile payment systems work?

Mobile payments rely on technologies like Near-Field Communication (NFC), QR codes, or mobile wallet apps. Behind the scenes, encryption, tokenization, and secure payment gateways ensure that sensitive information (such as credit card numbers) is protected during the transaction.

-

Mobile payment systems connect your mobile device with a merchant’s POS system. Once initiated, the payment request is communicated to the payment processor, which verifies the payment method and completes the transaction securely.

According to Juniper Research, NFC-based mobile payment transactions are expected to reach $4.5 trillion globally by 2023, further highlighting the dominance of contactless payments in the mobile landscape.

The growth of mobile POS Systems

For developers and product managers, the rise of mobile POS (mPOS) systems offers new flexibility in how businesses accept payments, freeing them from the constraints of traditional registers. But what is a mobile POS? It’s simply a mobile device—like a smartphone or tablet—that acts as a portable register, enabling businesses to process transactions anywhere, anytime.

In 2022, mPOS payments exceeded $3 trillion globally and are expected to reach $5.9 trillion by 2027, driven by the growing popularity of mobile devices and the need for businesses to adapt to flexible payment solutions.

Imagine running a pop-up shop or market stall without the need for bulky payment terminals. With mPOS, businesses can accept card payments, digital wallets, and even send electronic receipts—all from a handheld device. This flexibility is a game changer for small and large businesses alike.

Opportunities in mobile payments

The rise of mobile payments presents several key opportunities for businesses and developers:

- Expanded Market Reach: Mobile payments enable businesses to cater to a global audience. In regions where credit cards may not be common, mobile wallets like Alipay and M-Pesa are helping businesses reach new customers. By 2025, digital wallet usage is expected to account for 52% of global e-commerce transactions, up from 41.8% in 2021.

- Seamless Customer Experience: Mobile payments provide customers with a frictionless buying experience, whether they’re paying online or in person. 85% of consumers say they prefer using digital payment methods due to convenience. Moreover, mobile payments integrate seamlessly with loyalty programs and apps, which increases customer satisfaction.

- Data Insights: Businesses using mobile payment systems can gather rich data on customer behaviour. This data, in turn, helps tailor marketing strategies and offer personalized promotions. According to McKinsey, companies using customer analytics are 23 times more likely to outperform competitors in customer acquisition.

- Increased Security: Mobile payments are often more secure than traditional payment methods, thanks to encryption, tokenization, and biometric verification.

Challenges to consider

Despite the opportunities, mobile payments come with their own set of challenges:

- Compatibility issues: Developers must ensure that mobile payment systems work across various devices, operating systems, and networks. Not all users are on the same platform, and integrating payment systems that are universally compatible is no small feat.

- Fraud risks: While mobile payments are generally secure, they are not immune to attacks. In fact, digital payment fraud increased by 70% from 2020 to 2021. Product managers must ensure that their mobile payment systems comply with industry standards like PCI DSS and incorporate the latest security measures.

- Regulations & privacy concerns: Navigating complex regulations across different markets can be challenging, especially when mobile payments are involved. Developers need to ensure that their payment systems adhere to changing regulations, such as GDPR in the EU and CCPA in the U.S.

The future of mobile payments

The future of mobile payments looks promising, with continued innovation on the horizon. Artificial Intelligence (AI) and Blockchain are poised to revolutionize the space further. AI can enhance fraud detection, while blockchain offers the potential for faster and more secure cross-border payments.

"By 2025, AI-driven fraud detection in mobile payments is expected to reduce fraudulent activities by 25%, saving businesses billions."

Wearables like smartwatches are also gaining traction as a new medium for mobile payments. By 2024, it’s estimated that 1.3 billion people will be using wearable devices for payments.

For developers and product managers, the message is clear: while mobile is the future, there are still uncertainties in the market. Mergers & acquisitions, cross-border expansion, and potential collaboration could shape different outcomes. Therefore, banks, merchants, investors, and tech leaders must monitor these developments closely. As an Aevi partner, you're one step ahead of whatever comes next in paytech.

As mobile payments continue to transform the way businesses and consumers interact, it’s crucial to have a flexible, efficient system in place to handle the complexity of these transactions — especially in-person.

At Aevi, our in-person payment orchestration platform ensures seamless integration across various payment methods, including mobile and contactless, all while optimizing transaction flows for businesses of any size. By streamlining the payment experience, we help you stay ahead in this fast-evolving landscape.

Discover how Aevi can elevate your in-person payment solutions — get in touch today to learn more!

Interested in reading more around this subject? Here are some useful articles…