Key Insights

-

Tokenization replaces sensitive card data with non-sensitive tokens, reducing the risk of breaches and helping merchants meet PCI compliance standards.

-

Credit card tokenization PCI compliance lowers merchants’ data security risks and simplifies audits by removing raw cardholder data from their systems.

-

Payment enablers benefit from tokenization by limiting liability across their payment ecosystem and offering a secure, trusted solution to merchants.

-

Understanding the difference between tokenization and encryption is key - tokenization fully replaces data, while encryption scrambles it, making tokenization harder to exploit.

-

Aevi’s cloud-based platform offers secure, PCI DSS-compliant tokenization, supporting card-on-file, recurring payments, and flexible transactions across multiple channels.

Don't have time to read more now? Sign up to our newsletter to get the latest insights directly in your inbox.

Instead of your merchants storing a customer’s actual credit card number, tokenization works when their ePOS system instantly replaces the numbers with a random string of characters - something meaningless to hackers and useless if stolen. The real data? Locked away in a cloud-based vault. Tokenization, therefore, is an invisible but powerful layer of protection that keeps sensitive payment information safe without disrupting the transaction experience.

As a payment enabler, understanding how tokenization works can help you better support your merchants in reducing risk and simplifying compliance, resulting in secure, trusted payments. Let’s explore how tokenization protects card data, the key benefits for your merchants, how it compares to encryption, and where it’s being used - from card payments to blockchain tokenization.

What is tokenization?

Tokenization, introduced in the early 2000s in response to rising concerns about payment data security and PCI DSS compliance, is a data security method that replaces sensitive information, such as credit card numbers, with unique, non-sensitive tokens. These tokens hold no exploitable value on their own, but they allow businesses to process payments or store data securely without exposing the original information.

What is tokenization used for? It’s commonly applied in card payments, digital wallets, and increasingly in blockchain-based transactions. Unlike encrypted data, tokens cannot be reversed back to their original form without access to a secure token vault, which adds an extra layer of protection.

There are several approaches to tokenization, each offering different levels of flexibility, security, and control - here’s how gateway, pass-through, and payment service tokenization compare:

- Gateway tokenization

Gateway tokenization allows merchants to store card data via a payment gateway, which returns a token for future transactions. However, each gateway uses its own token format, locking merchants into that provider and making switching gateways costly and complex.

- Pass-through tokenization

Pass-through tokenization sits between the merchant and gateway, enabling flexible token use across multiple platforms and payment types without altering existing code.

- Payment service tokenization

Payment service tokenization offers a single API for routing payments to multiple gateways. It’s ideal for businesses with complex needs and removes gateway control over tokens, improving flexibility, security, and reducing PCI scope.

Without tokenization, businesses would need to store actual card numbers, which creates a much higher risk if their systems are ever breached. One weak spot could expose thousands of customer details. Tokenization helps prevent this by ensuring that even if someone gets hold of a token, it’s useless on its own and can’t be used to make a payment or steal information.

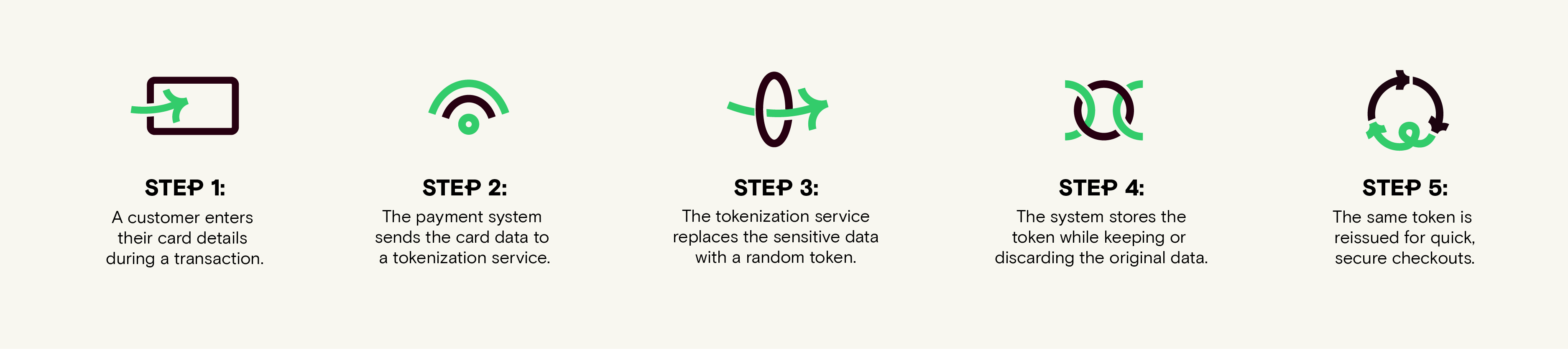

How does payment tokenization work?

Here’s how tokenization typically works in the context of credit card tokenization PCI compliance:

- A customer enters their card details during a transaction.

- The payment system sends this data to a tokenization service.

- The sensitive card data is replaced with a token - a string of random characters.

- The token is stored and used for future transactions, while the original card data is securely stored in a token vault or never retained at all.

- If that customer comes back to buy something else, the tokenization system can issue the same token for that card, depending on how it's set up. This allows businesses to recognize returning customers and offer quick, secure checkouts without ever needing to store the original card data.

For merchants, this process is vital because handling raw cardholder data comes with significant security risks and strict regulatory requirements. By using tokenization, they avoid storing sensitive information directly, reducing the impact of a potential breach. This also helps them meet PCI DSS compliance standards, which are designed to protect card data and minimise security threats. In many cases, tokenization lowers the scope of PCI compliance, saving time, resources, and reducing exposure to non-compliance penalties.

As an example of tokenization in practice, at Aevi, we use tokenization to replace sensitive card data - like PANs - with unique tokens that can be securely stored and processed. Behind the scenes, our system maintains an encrypted database of PAN-token pairs. Active records are kept in a current table, while older data is archived annually and retained for up to 10 years for compliance.

Each token is 21 characters long, uniquely generated, and structured in a way that prevents manual entry errors. When it comes to settlements, our system retrieves tokens by matching the original PAN and issuer ID. For detokenization - when we need to convert transaction files like UDK or GMCIF back to PANs for acquirers - we follow strict encryption protocols and file renaming rules to ensure both security and compliance at every step.

What are the benefits of tokenization for payment enablers and merchants?

For ISVs, PSPs, and payment enablers, tokenization offers both technical and commercial advantages, but the benefits also extend directly to your merchants, making it a win-win.

For payment enablers, tokenization reduces your liability by limiting the exposure of sensitive data across your POS system. It helps streamline PCI DSS compliance, making audits less complex and costly, while offering a differentiator in your service offering. Payment solutions that include tokenization are more appealing to merchants who value security and compliance but may not have the infrastructure to manage it themselves.

For merchants, tokenization helps protect customer data and reduce the risk of breaches, which in turn improves operational trust. It also supports various types of payment methods and flexible payment models, such as recurring billing or card-on-file, without compromising data security.

Specific benefits include:

- Reduces the risk of data breaches, since tokens cannot be reused or exploited outside the environment they were created for.

- Minimizes PCI DSS scope by ensuring merchants don’t store raw card data, simplifying compliance and reducing costs.

- Supports recurring payments, subscriptions, and stored payment methods - ideal for SaaS, retail loyalty programs, and hospitality pre-booking.

- Improves customer trust with visible commitment to secure payments, driving higher retention and fewer abandoned transactions.

- Enables omnichannel payment flexibility, letting merchants accept payments online, in-store, or via app without added complexity.

Whether you're enabling payments for global retail, hospitality, or digital platforms, card tokenization helps ensure that sensitive data remains protected - benefiting your platform’s security, your merchants’ peace of mind, and your customers’ trust.

"Tokenization is a game-changer in payment security, replacing sensitive card data with unique tokens that are useless if breached. Unlike encryption, which scrambles data but can be decrypted, tokenization removes the original data from the equation entirely. As payments evolve, advancements like AI-driven fraud detection and quantum-safe cryptography will further strengthen tokenization, making transactions even more secure and compliant."

Miroslav Pekarek, CPO, Aevi

What’s the difference between tokenization and encryption?

Following on from the benefits of tokenization, it's worth addressing a common point of confusion: what is the difference between tokenization and encryption?

While both are used to protect sensitive data, they work in fundamentally different ways. Encryption converts data into a coded format using an algorithm and a key. The data can be decrypted and read again, as long as the key is available.

Tokenization, on the other hand, replaces the data entirely with a token and stores the original information securely elsewhere. Without access to the token vault, the token is meaningless and cannot be reverse-engineered.

In the context of payment security, tokenization often offers stronger protection because it removes sensitive data from your systems altogether, making it a highly effective method for reducing risk and simplifying compliance.

Tokenization and PCI compliance

Tokenization is a major asset in achieving and maintaining PCI compliance. By replacing sensitive cardholder data with tokens, businesses can significantly reduce their PCI DSS compliance requirements and protect themselves from fines, fraud, and reputational damage.

PCI DSS even recognizes tokenization as a method to minimize data storage risks and simplify audits. Credit card tokenization PCI compliance is especially important for businesses offering card-on-file, recurring billing, or omnichannel payments.

What is blockchain tokenization?

Beyond payments, what is blockchain tokenization? In blockchain, tokenization involves converting real-world or digital assets (like property or art) into digital tokens stored on a blockchain.

While payment tokenization secures transactions, blockchain tokenization focuses on creating digital ownership of assets, enabling trading and transfer via decentralized platforms. Both share the principle of replacing sensitive data or assets with unique tokens, but their applications are different. You can read more about this in our article ‘Security of Crypto Payments’.

How Aevi’s cloud-based in-person payment platform supports tokenization

As data security threats continue to evolve, tokenization remains one of the most effective ways for businesses to protect payment data, reduce risk, and meet compliance requirements. It not only safeguards sensitive information but also helps build lasting trust with customers who expect their data to be handled securely.

Aevi’s cloud-based in-person payment platform makes it easy to implement tokenization without adding complexity. By supporting secure, PCI-compliant tokenization at the core of your payment stack, Aevi helps you protect cardholder data, reduce the scope of compliance, and enable secure payment flows across multiple channels.

Whether you need to support card-on-file, recurring billing, or global transactions, Aevi’s device-agnostic platform allows you and your merchants to handle tokenized payments with confidence, backed by advanced encryption, secure APIs, and real-time control over transactions.

Here are some of the specific ways Aevi’s software enables tokenization to support you, your merchants and their customers…

Aevi’s tokenization approach allows businesses to protect payment data, streamline transactions, and gain valuable insights, without the compliance headaches of storing sensitive card details. We act as a secure intermediary, enabling merchants to use tokenization in a way that fits their payment strategy, whether through acquirers, third parties, or network tokens.

Looking for a smarter, secure way to manage tokenization? Aevi has you covered. Let’s talk.

Interested in reading more around this subject? Here are some useful articles…