Key Insights

-

BNPL (Buy Now, Pay Later) is transforming consumer finance by offering flexible, interest-free payment options that appeal to younger shoppers.

-

Retailers see higher sales and conversions by offering BNPL, but must balance the associated costs and risks.

-

Payment orchestration optimizes the BNPL experience by streamlining payment methods, reducing costs, and ensuring compliance.

Don't have time to read more now? Sign up to our newsletter to get the latest insights directly in your inbox.

In recent years, the Buy Now, Pay Later (BNPL) model has taken the retail and finance worlds by storm. This innovative approach to consumer financing allows shoppers to purchase goods and services immediately while spreading the cost over a set period, often without interest.

The US boasts the largest BNPL market by value, while China leads in market volume. Notably, Sweden has the highest BNPL penetration rate, with BNPL accounting for 25% of all e-commerce sales in the country.

The BNPL market has surged due to shifting consumer preferences and the rise of e-commerce, attracting younger consumers with its deferred payment options. However, as banks and retailers join the market, it faces challenges from potential regulations and high interest rates. To remain competitive, BNPL providers must adapt by offering value-added services and expanding into broader financial services.

So, why is BNPL trending, how does it work, what are its benefits and drawbacks, and what does the future hold for this rapidly growing sector?

What is BNPL?

BNPL is a type of short-term financing that allows consumers to make purchases and pay for them in installments over time. Unlike traditional credit cards, BNPL options typically come with interest-free periods, making them an attractive alternative for many shoppers. Leading pureplay BNPL providers include Klarna, Afterpay, Affirm, and Walmart’s One. Additionally, several banks and other Payment Service Providers (PSPs) offering BNPL options are PayPal, HSBC, Citi, JPMorgan Chase, CommBank, and Monzo.

What are the key characteristics of BNPL?

- At checkout: When shopping online or in-store, consumers select the BNPL option at checkout.

- Payment schedule: The total purchase amount is divided into a series of smaller, manageable payments, usually spread over a few weeks or months.

- Automatic deductions: Payments are automatically deducted from the consumer's bank account or charged to their credit/debit card as per the agreed schedule.

- Instant approval: Approval for BNPL is typically instant, with minimal credit checks, making it accessible to a wide range of consumers.

- Customer journey: Throughout the payment period, consumers can track their payment schedules and remaining balances via the BNPL provider's app or website, ensuring a seamless and transparent experience.

What are the differences between online and in-person BNPL?

When it comes to BNPL transactions, the process and user experience differs between online and in-person shopping.

- Online BNPL transactions: These are designed to be seamless and are directly integrated into retailers' payment systems. Consumers simply select the BNPL option at checkout, providing their personal and debit card details. This streamlined process makes it quick and convenient for users to make purchases without leaving the retailer's website.

- In-store BNPL transactions: For in-person shopping, consumers need to use the BNPL provider's app, which generates virtual cards or QR codes for the transaction. These virtual cards can be added to mobile wallets for contactless payments, and they are often single-use, providing an extra layer of security.

Additionally, some BNPL companies offer physical cards. Unlike virtual cards, obtaining these requires a more formal application process and a strong credit profile for approval, similar to traditional credit card applications.

Overall, while online BNPL transactions emphasize ease and integration, in-store BNPL options focus on flexibility and security, offering both virtual and physical card solutions to suit different consumer needs.

Why is BNPL so popular?

- Financial flexibility: BNPL provides consumers with greater financial flexibility, allowing them to manage their cash flow more effectively without the burden of high-interest debt.

- Enhanced shopping experience: By offering a seamless and convenient payment option, retailers can enhance the shopping experience, potentially increasing customer satisfaction and loyalty.

- Attracting younger consumers: Millennials and Gen Z, who may be wary of traditional credit cards, find BNPL appealing due to its straightforward terms and lack of hidden fees.

- Boosting sales: Retailers benefit from higher conversion rates and increased average order values, as BNPL encourages consumers to make larger purchases.

The benefits of BNPL:

- Interest-free periods: Many BNPL services offer interest-free periods, making it a cost-effective option for consumers who pay on time.

- Easy access: With minimal credit checks and instant approval, BNPL is accessible to a broad audience.

- Improved budgeting: The structured payment schedule helps consumers budget and plan their expenses more effectively.

The drawbacks of BNPL:

- Potential for overspending: The ease of using BNPL can lead to overspending and accumulation of debt if consumers are not careful.

- Lack of trust: Some customers may be skeptical about BNPL services due to concerns about hidden fees, potential impact on their credit scores, or lack of transparency in the terms and conditions. Additionally, there are those who prefer not to borrow money when making a purchase, choosing instead to pay upfront to avoid debt and financial obligations.

- Late fees: Missing a payment can result in significant late fees, which can add up quickly.

- Credit impact: BNPL services typically involve soft credit checks, but missed payments can still negatively impact a consumer's credit score, especially for younger customers with less disposable income and multiple sources of debt. In some countries like Germany, using BNPL services like Klarna may result in data being saved by credit bureaus like SCHUFA, potentially complicating future credit applications and contributing to the "debt trap" for young consumers. Additionally, BNPL data may not be processed responsibly by outdated credit models in the US, potentially lowering credit scores due to their inability to properly assess BNPL repayment behaviors.

- Regulatory scrutiny: As BNPL grows in popularity, it faces increasing regulatory scrutiny to ensure consumer protection and fair practices.

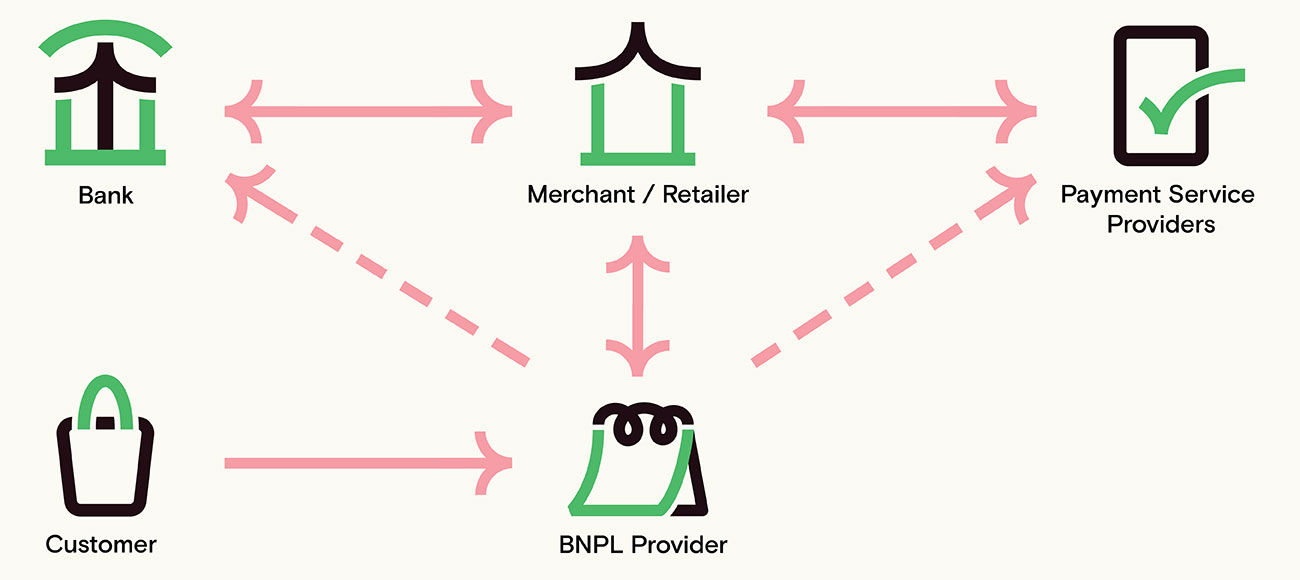

BNPL in the payments value chain

Merchants/Retailers:

- Benefits: Merchants experience higher sales and improved conversion rates by offering BNPL options, attracting younger customers who prefer flexible payment methods.

- Costs and risks: They pay higher fees to BNPL providers but avoid credit and fraud risks associated with traditional credit cards.

- Competitive edge: Offering BNPL helps retailers stay competitive in the market and differentiate themselves by catering to modern consumer preferences for convenience and financial flexibility.

Customers:

- Benefits: Customers enjoy convenient, mobile payment options without the need for physical cards, often utilizing QR codes or digital wallets. BNPL offers interest-free installment payments, quick approval processes without hard credit checks, and flexibility in managing payments.

- Challenges: There is a risk of overspending and accumulating debt if not managed responsibly, especially for younger consumers with less financial experience.

BNPL providers:

- Role: BNPL providers facilitate sales transactions between merchants and customers.

- Revenue model: They earn revenue from merchant fees and late fees, assuming the credit risk associated with deferred payments.

- Financial challenges: Providers face higher operational costs with rising interest rates and regulatory scrutiny.

- Diversification strategies: To succeed and differentiate themselves, BNPL providers are exploring new revenue streams such as integrating with marketplaces and offering traditional financial services.

- Innovative practices: Some providers are becoming shopping destinations by allowing merchants to advertise on their platforms. They also focus on mastering customer journeys in specific product categories to enhance their value proposition.

Banks/Merchant Acquirers:

- Entry into BNPL: Banks and merchant acquirers are entering the BNPL space to leverage their existing customer base and infrastructure.

- Strategies: They develop their own BNPL products or partner with existing providers to capture a share of the growing market and diversify their payment offerings.

- Competitive advantage: This move helps them stay competitive and meet the evolving demands of consumers seeking flexible payment options beyond traditional credit cards.

Payment Service Providers (PSPs)/ISOs/ISVs:

- Benefits: PSPs, ISOs, and ISVs benefit from strong merchant relationships that they can strengthen by offering BNPL as part of their service portfolio.

- Cost and flexibility: ISOs and ISVs often operate with lower overhead costs compared to banks, allowing them to potentially offer more competitive rates and terms to merchants and consumers.

- Market opportunity: BNPL integration enhances their service offering, catering to the demand for flexible payment solutions in various industries.

The future of BNPL

The BNPL market is expected to continue its rapid growth, driven by ongoing consumer demand and retailer adoption. Here are some trends to watch:

- Increased competition: More players are entering the BNPL space, from fintech startups to established financial institutions, driving innovation and competitive offerings.

- Regulation and compliance: As BNPL becomes more mainstream, regulatory bodies are likely to impose stricter guidelines to protect consumers and ensure fair lending practices.

- Expansion beyond retail: BNPL services are expanding into new sectors, including travel, healthcare, and education, providing consumers with more opportunities to finance their purchases.

- Technological advancements: Integration with emerging technologies, such as artificial intelligence and machine learning, will enhance the BNPL experience, offering personalized financing options and improved risk management.

From 2023 to 2024: What's changed and what has not?

The Buy Now, Pay Later revolution is far from over. As this innovative financing model continues to gain traction, the future holds exciting possibilities. We can expect to see increased competition and innovation within the BNPL space, driven by both fintech startups and traditional financial institutions. Regulatory frameworks will likely evolve to ensure consumer protection and fair lending practices.

Furthermore, BNPL services are set to expand beyond retail into sectors like travel, healthcare, and education, providing consumers with even more financing options. Technological advancements, particularly in artificial intelligence and machine learning, will enhance the BNPL experience, offering personalized financing solutions and better risk management. As we move forward, BNPL will play a crucial role in shaping the future of consumer finance, offering greater flexibility and convenience for shoppers worldwide.

Source: Capgemini Research Institute for Financial Services analysis, 2023

As the BNPL market expands, payment orchestration plays a crucial role in its integration by simplifying and managing the growing array of payment providers and methods. By incorporating BNPL into a centralized orchestration platform, businesses can enhance the customer experience through seamless and streamlined payment processes while optimizing transaction costs. This integration allows merchants to easily offer flexible payment options like BNPL without adding complexity to their systems. Moreover, payment orchestration provides real-time insights and helps navigate compliance requirements, ensuring that BNPL transactions are handled smoothly and efficiently in response to evolving consumer demands for alternative financing solutions.

Interested in reading more around this subject? Here are some useful articles…