What is the difference between a merchant acquirer and a payment processor?

- Thought leadership

- 5 Minute Read

- Last updated 10/07/2023

In the payment stack, acquirers, processors, and platforms play distinct roles across risk, settlement, and transaction handling. The payment facilitator model sits between merchant and acquirer, and as the payment facilitator role grows, understanding who owns what becomes essential to building scalable, well-governed payment setups.

Key Insights

- The merchant acquiring process spans onboarding, underwriting, monitoring, and fund movement, making it a commercial and regulatory function as much as a technical one.

- Confusion between merchant acquiring and processing often leads to gaps in accountability when issues arise.

- A payment facilitator simplifies access to payments by aggregating merchants under a single agreement, trading individual control for speed and scale.

- As payment stacks become more modular, understanding who owns which part of the flow matters more than the technology itself.

- Clear separation of roles helps merchants and platforms build setups that scale without losing control, visibility, or accountability.

Don't have time to read more now? Sign up to our newsletter to get the latest insights directly in your inbox.

What is a merchant acquirer?

A merchant acquirer, typically a bank, fulfils a crucial role in handling a merchant’s payment card transactions. They hold the merchant account and receive the deposits from sales. With a direct relationship with card networks like Visa and Mastercard, the acquirer enables merchants to process card transactions on these networks and assumes financial responsibility for the activity. The acquirer acts as an intermediary, processing and settling transactions with the card issuer or association. To uniquely identify payment transactions, merchants are assigned a Host Merchant ID or a similar identifier by the acquirer. While banks commonly serve as acquirers, other entities such as loyalty card acquirers, fleet card acquirers, or store/retailer acquirers can also fulfil this role.

What is a payment processor?

A payment processor (or sometimes “sub-acquirers”) will likely be a technology company, with the infrastructure to authorise transactions and move them from the merchant, through the card networks to a consumer’s bank and back again. Payment processors manage the process of moving the funds from the customer’s bank to a merchant bank. Its role is similar to that of an acquirer, but it doesn’t completely replace it. Thus, it can be also understood as a kind of intermediary player between the acquirer and the store.

-

What is the issuing bank?

The issuing bank refers to the bank or financial institution responsible for providing debit, credit, or prepaid cards to consumers on behalf of the card networks. It acts as an intermediary between cardholders, networks, and acquirers. The issuing bank’s role is crucial in determining whether a customer’s payment is accepted, as the information sent from the issuing bank validates the transaction. While consumers may believe that their credit cards are issued by MasterCard or Visa, these companies are payment transaction processors and not direct issuers of credit/debit cards.

The issuing bank is also responsible for billing and collecting funds for purchases made using the card. In the payments value chain, the card issuer pays the acquiring bank for the cardholder’s purchases, and the cardholder repays the issuing bank according to the terms of their agreement.

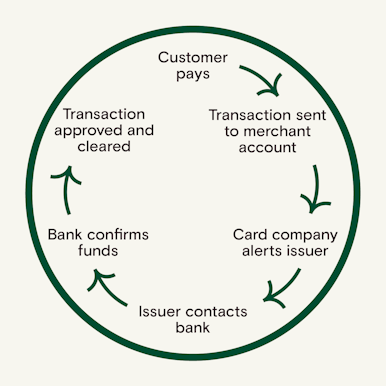

The payment chain

For a little more clarity, let’s look at the payment chain in action.

-

- The customer pays via their debit or credit card.

- The transaction travels to your merchant account (provided by your merchant acquirer), where it waits for approval.

- The card company providing the customer’s card is alerted about the purchase.

- The card company contacts the customer’s bank (the issuing bank) to ensure enough money is in the account.

5. The customer’s bank tells the card company that the funds are there to afford the purchase.

6. The card company approves the transaction and the transaction remains in your merchant account while it’s been cleared.

Your merchant acquirer is responsible for providing your merchant account and giving you the capabilities to run card transactions. It is the payment processor that then facilitates each step of the above process and makes things happen.

Can the same entity be both a merchant acquirer and payment processor?

Often, the same entity provides both functions. Acquiring banks often offer payment processing as part of their service to clients. On the other hand payment processors can provide merchants with access to accounts through their existing relationships with acquiring banks.

If you can opt for a provider that offers both services, it eliminates the need to choose a suitable provider for each.

What are ISOs?

You may have seen the term ISO too. We’ll take a quick look at what this is, as well as detailing the difference between Retail ISOs and Wholesale ISOs.

ISO refers to an independent sales organisation and is effectively an intermediary that signs up merchants for an acquirer’s payment processing services. A Retail ISO is a simpler function and exists to source merchant customers on behalf of the merchant acquirer. Wholesale ISOs on the other hand still work on behalf of the acquirer but they take on many of the responsibilities of payment processing too. Ultimately, however, the bank is responsible for the movement of funds and any potential losses. The acquirer is therefore still a key piece of the relationship.

Today, however, ISOs are beginning to be phased out and be replaced by payment facilitators (PayFacs).

Feature/Responsibility

Acts as an intermediary for the acquirer

Signs up merchants

Sources merchant customers only

Handles underwriting, risk, and operational responsibilities related to processing

Manages onboarding beyond sales

Works on behalf of the acquirer

Holds responsibility for movement of funds

Bears financial risk and losses

Bank remains ultimately responsible

Role being phased out in favor of PayFacs

Retail ISO

✓

✓

✓

✗

✗

✓

✗

✗

✓

✓

Wholesale ISO

✓

✓

✗

✓

✓

✓

✗

✗

✓

✓

What is a payment facilitator?

A PayFac is a company that provides the infrastructure for businesses (referred to as sub-merchants) to begin accepting card payments. The PayFac will onboard and underwrite the sub-merchant and provide the technology needed to process electronic payments and receive the funds. They do the following:

- Onboard sub-merchants and perform full underwriting

- Monitor transactions for anomalous or suspicious behaviour

- Provide the funds to sub-merchants and reconcile their transactions

- Manage the chargeback process alongside the acquiring bank

For a payment facilitator to be able to function, they need two key relationships. The first is with an acquiring bank and the second is with a payment processor.

When you set up your business to take payments, it’s crucial to understand the steps in the process and to work with the appropriate entities to ensure it is a seamless process for your business and your customers. At Aevi, we work with merchant acquirers, specialist payments services providers (PSPs), ISVs, ISOs and financial institutions. Our platform is open, device-agnostic, and flexible. It enables payments and data to flow through any channels that may be required. It allows the entire payment chain to evolve.

Discover more about Aevi and what our platform can mean for the future of your business.

Interested in reading more around this subject? Here are some useful articles…